Definition: A step-wise cost, also called a stair-step cost, is an expense that stays constant over a range of production and changes in lump sums as production volumes increase and decrease. In other words, these costs remain fixed over a relevant range of production volume. When the production volume changes outside of the relevant range, the costs increase or decrease in a step fashion.

Example

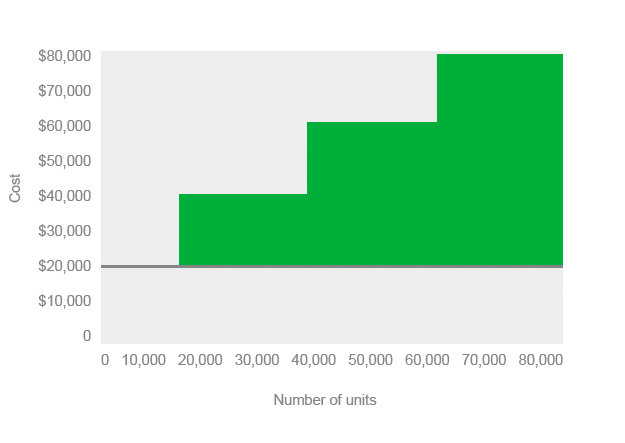

It might be easier to explain a step-wise cost with a diagram example. Here’s what a step cost graph looks like.

As you can see, the costs remain constant over a range of production and then steps up to the next cost level as production exceeds the relevant range. For instance, this company incurs $40,000 of expenses if it produces 15,000 units or 40,000. The costs jump up to $60,000 once the company produces 40,001 units. This cost level remains constant up to 65,000 units until it steps up to the next range.

An example of a step cost might be a factory’s production supervisors’ salaries. As the factory production increases, it hires more supervisors to oversee the workers and operations. These supervisors are capable of overseeing a range of production volumes. Think about this concept with the graph above.

What Does Step-Wise Cost Mean?

The company can employ one supervisor to oversee the production volumes between 15,000 units and 40,000 units. After 40,000 units, one supervisor can’t oversee the operations. Another supervisor must be added, so between volumes of 40,001 and 65,000 units two supervisors must be hired. After the company starts producing more than 65,000 units, two supervisors will not be able to keep up with the production volume. Another supervisor must be hired.

As each supervisor is hired, the costs incrementally increase in a step fashion. They don’t gradually increase with production levels like variable costs.